Saturation DER Modelling

Solar and batteries put the duck curve to sleep

This article was published in IEEFA Asia Pacific and is courtesy of Dr Gabrielle Kuiper.

27 Apr 2023

Modelling plays a central role in planning for the future of Australia’s energy markets. It’s a problematic tool given all modelling is based on the past and we know the future will be dramatically different.

Sometimes it’s worth turning a tool on its head to create fresh understanding.

ITP Renewables has done this by ‘backcasting’ scenarios for saturation levels of distributed energy resources (DER). In other words, rather than model scenarios based on forecast energy needs, on my suggestion ITP Renewables started with the inevitability that some day we will reach saturation DER, and modelled what this would mean for the electricity system.

We know that eventually every rooftop in the National Electricity Market (NEM) that can have solar, will. We know solar households will most likely have batteries, and potentially will be able to trade electricity easily with their neighbours. They will also be all electric, with flexible demand in the form of controlled loads able to be time-shifted, and have electric vehicles (EVs) that can charge in the daytime or overnight. We’ll also have community batteries in some form.

We don’t know when this will happen, but ITP modelled what this might look like through a range of scenarios, starting with 70% of houses with solar, then adding different varieties of DER in sequence (e.g. batteries, controlled loads, EVs) to examine the impacts on solar photovoltaic (PV) exports, PV export peaks, network peaks and high spot price periods (4–8pm).

This approach to modelling gives a sense of the consequences for electricity flows locally and through the broader grid for a saturation DER suburb in a way that iterative modelling from the past is unlikely to do.

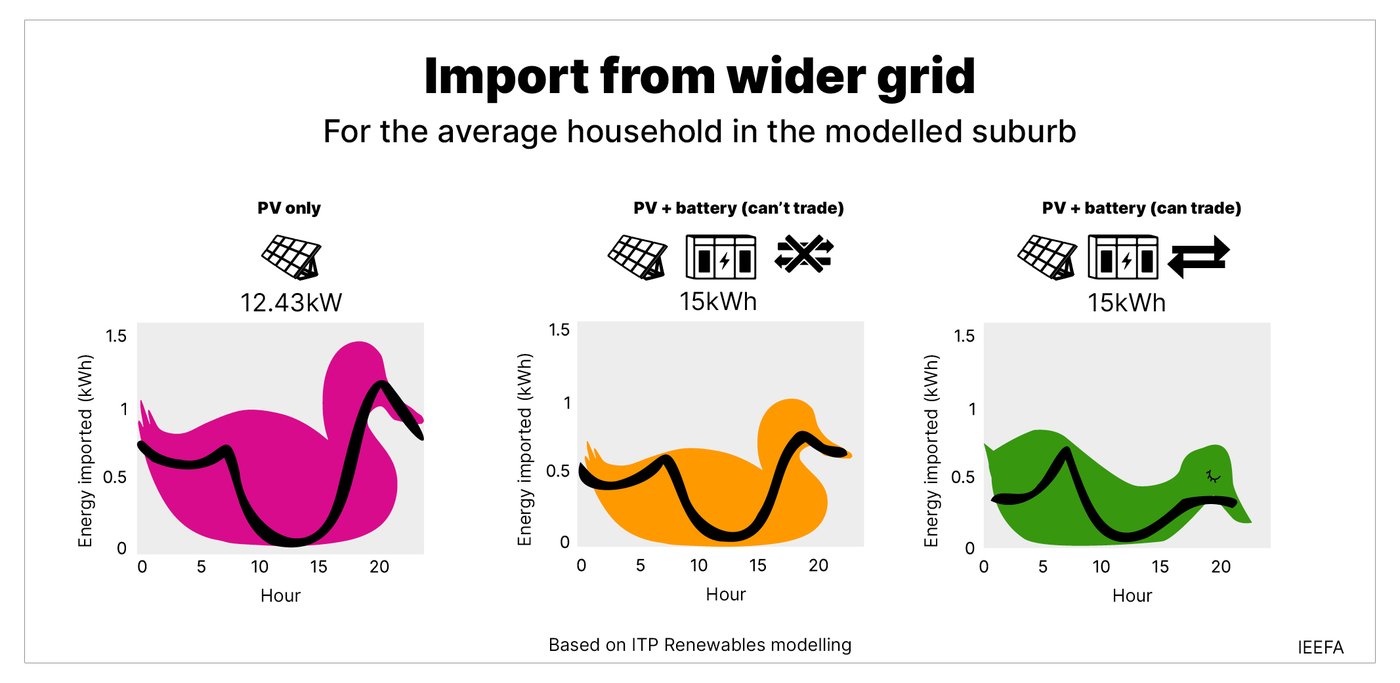

The most significant finding from this fresh approach is that rooftop solar plus batteries will put the famous solar-created supply-demand duck curve (Figure 1) to sleep.

Figure 1 shows three scenarios for the load of an average household in the modelled suburb: PV only (with average PV system size of 12.43kW); PV plus battery storage with no battery trading (with average PV + battery system size of 15kWh); and PV plus battery storage with battery trading within the suburb with no friction and at no net cost (with average PV + battery system size of 15kWh).

The black line in the figure shows the imports from the wider grid into the household for the three scenarios. This illustrates the change by scenario – from a big fat-bellied duck to a sleeping one.

The significance of a sleeping duck is twofold – it dramatically reduces the abundant belly of solar generation during the middle of the day and there is no steep ramp rate to the head of the duck in the evening peak. In fact, there is no evening peak. Across all the modelled scenarios, rooftop solar plus battery trading (third graph in Figure 1) reduces the 4–8pm wholesale market evening peak by 67–92%.

How much and how fast the duck sleeps will depend a lot on the number and size of batteries and EVs per household and the regulations for trading this capacity. The more batteries and flexible load in the system, the greater the likelihood of a sleeping duck – that is, a flatter grid demand/supply curve.

Regardless, the 4–8pm peak is the time where generators have traditionally earnt the bulk of their revenue. If this peak no longer exists, there will likely be significant impacts on the spot market.

At the same time, concerns about managing minimum demand on the grid in the middle of the day are eased (minimum demand increases by 21% in the scenario where batteries can trade). Similarly, concerns about the afternoon ramp rate are also reduced (afternoon ramp rate decreases by 17% in the battery trading scenario). The logical consequences should be significant downward pressure on wholesale spot prices, providing benefits for all consumers.

Despite the recent increases in wholesale electricity market prices, the costs for the local poles and wires (the distribution network) have always been the largest component of household customers’ electricity bills. Over the last two decades, distribution networks in Australia have generally been built to meet summer evening air-conditioning peaks. The $82.6 billion collective value of the regulated asset bases of distribution network service providers (DNSPs) in the NEM is largely based on their capacity to supply electricity from the grid at these peak times.

Rooftop solar exported back into the grid reduces the need for distribution network capacity. In the modelled suburb, solar PV alone reduces the average summer network peak by 28% and moves it 2.5 hours later in the day. In the third scenario where local ‘trading’ is made ‘frictionless’, household batteries reduce the average summer network peak by 64%, more than half. The summer network peak reduction figures are less than the average wholesale evening peak reductions because they are based on five specific events throughout the year.

Of course, there will also be winter peaks, which will change, especially in southern states such as Victoria, as heating switches from gas to electricity, and networks will need to consider this location-specific issue.

In general, however, the implications of these changes to network peaks are that DNSPs should not be arguing for increased network investment to cope with increasing electricity flows from DER. Instead, they should be arguing for increased software investment to help facilitate these flows on their networks.

All Victorian DNSPs have received approved expenditure for such investments, in particular Dynamic Voltage Management Systems (DVMS) and DER Management Systems (DERMS). Such smart software systems can be cost-effectively combined with traditional tools that quickly and cheaply enable more solar in the system, such as transformer tap changes at substations.

One interesting trial is Project Edith, which is looking at the use of real-time network pricing to this end. Real-time network pricing is far more thoughtful than bluntly charging solar customers to export excess solar to the grid, which this analysis suggests would be perverse given the benefits PV can provide to networks.

Overall, with decreased network peaks driven by solar and battery uptake, reduced capital expenditure would seem logical, and with that, lower distribution charges for customers. The system-level benefits of DER should be passed on to all customers. This requires the Australian Energy Regulator to understand this modelling and, preferably, to adapt distribution revenue regulation to meet the new circumstances of growing levels of DER. Ideally, the Australian Energy Market Commission would rethink revenue regulation from first principles given the dramatic changes coming in distribution networks.

Saturation levels of rooftop solar will create a large low belly in the duck curve. Without large load shifting, we won’t make the most of the abundant solar generation in the middle of the day. There are many solutions to this challenge.

Shifting controlled load to the middle of the day has limited benefits with the currently low levels of controlled demand in most states. In Victoria, South Australia and much of New South Wales, however, there is a large opportunity to switch from gas to smart (controllable) electric hot water, which can be heated by solar electricity in the middle of the day.

Queensland’s Ergon and Energex already have 850 megawatts of controlled demand in both hot water and air-conditioning systems. The state has a huge head start on the demand flexibility needed to optimise variable renewable energy generation and consumption, yet Energy Queensland has recently implemented rooftop solar cutoffs for systems over 10kVA meaning they can switch off these systems when requested by the Australian Energy Market Operator (AEMO).

While behind-the-meter (BTM) batteries and load shifting can soak up some of the midday sun, the other big opportunity is in daytime EV charging. In a separate scenario for households with PV, batteries and daytime EV charging saw a 47–84% increase in minimum demand from the wider grid. This shows that we need to get smart EV charging standards into the NEM as soon as possible.

It’s worth noting that none of the scenarios modelled were designed to optimise outcomes across the electricity system or for consumers. They were simply different combinations of technology and enabling conditions. We could create even better outcomes if we plan for them.

From the insights of ITP Renewable’s saturation DER modelling, there are some clear policy directions for the Commonwealth’s energy performance strategy and state governments’ DER policies and programs.

Policies and programs should aim to maximise flexible demand, especially shifting water heating with controlled load to the middle of the day and assisting consumers to switch from gas to smart electric hot water systems.

DNSPs should be looking at matching renewable resources and network capacity by location for EV charging. It’s not clear any organisations are taking a system-optimisation view of EV charging and there’s a danger that the lack of EV charging standards and coordination will end up increasing overall costs for consumers. The modelling also looked at scenarios involving ‘neighbourhood’ batteries and further investigation is needed into how these can be used for the greatest benefit for consumers, as opposed to the DNSPs.

Projects Edith, Edge and Symphony have begun to experiment with targeted remuneration for DER services within a local network area. DNSPs should continue to support this evolving work and the energy market institutions need to ensure consumers can be compensated for the services their BTM devices can provide to the grid.

Finally, AEMO’s next Integrated System Plan (ISP) should revise its DER uptake forecasts and attempt integrated planning with distribution networks. In particular, the ISP should model as many different scenarios for DER as it does for large-scale renewables. In general, we need energy system and market planning to better understand the implications of high levels of DER on the need for large-scale generation and storage.

DER saturation modelling has shown that DER has the ability to reduce peak demand in networks if managed well with significant implications for network capital expenditure requirements. In aggregate, DER also has the ability to bring down wholesale electricity prices. Given the delays to transmission builds and the Snowy 2.0 project, there should be greater focus on taking this ‘small stuff’ seriously and designing the policies, programs and regulations that will mean growing levels of DER will result in lower costs for all consumers. The ITP Renewables modelling shows saturation DER could benefit all consumers, including those without rooftop solar, if we get the policy and regulatory settings right.